The latest edition of the TransUnion CIBIL Credit Market Indicator (CMI) report specifies that credit demand in the quarter ended March 2023 remained robust, rising across almost all product types, except for home loans.

Further, according to the report, unsecured credit portfolios continue to scale up, backed by small-ticket loans. “Digital and information-oriented lending is fuelling the growth of retail credit, especially in unsecured consumption-led products, which grew at a compound annual growth rate (CAGR) of 47 percent from the quarter ended March 2021 to March 2023,” said Rajesh Kumar, MD and CEO of TransUnion CIBIL.

Home loan segment witnessed lower demand

Insights show that other than mortgage loans, all credit products enjoyed double-digit growth (see graphic). However, the slump in home loans is specifically in the affordable housing segment (home loans with a sanctioned amount below Rs 25 lakh). This segment witnessed a year-on-year drop of 16 percent in the number of loan accounts opened and a 15 percent drop in the sanctioned amount. On the contrary, home loans with the amount sanctioned above Rs 25 lakh experienced growth of 1 percent in volume and 6 percent in value terms.

“The approval rates were lower compared to the same time in the prior year. Lenders were being cautious on default on home loans, with interest rates rising,” Kumar explained.

ALSO READ: Inoperative PAN is not inactive PAN, clarifies I-T Dept amid concerns on ITR filing

Lower approval rates for credit to new-to-credit (NTC) consumers

Sachet sized financial products, which comprise smaller loans of less than Rs 50,000, are increasingly becoming popular as they are affordable and easier to access. These products have fuelled credit adoption among new-to-credit (NTC) consumers and underserved consumers in semi-urban and rural areas.

ALSO READ: ITR filing: Who can file ITR-2 and who cannot

There is a lower approval rate among NTC consumers, whom lenders typically approach with caution: approval rates for these consumers have reduced from 34 percent and 28 percent in March 2020 and 2021, respectively, to 23 percent in the quarter ended March 2023.

“A significant opportunity exists in accelerating financial inclusion given India’s low credit penetration and large young population. Identifying and providing access to credit to India’s deserving young consumers creates pathways for long-term and sustainable credit growth,” Kumar said.

“Today, technology can play a pivotal role in mitigating the risk associated with the NTC segment. Innovative use cases are being explored to identify patterns of risky behaviour and proactively intervene to prevent defaults,” Anand Agrawal, Co-Founder & CPTO of Credgenics, a loan collections and debt resolution technology platform, said. He added that early identification and personalisation of strategies goes a long way in resolving default cases at an early stage.

ALSO READ: The variety in banking and financial sector mutual funds and which one to pick

Recently, advanced data-backed systems powered by machine learning capabilities have helped many banks, non-banking finance companies (NBFCs) and fintechs transform their loan collection approach with holistic segmentation, actionable insights, borrower behavioural indicators, and personalisation strategies for debt resolution.

“Lenders need to empower their NTC consumers with personalised financial guidance to prevent defaults and resolve cases amicably,” Agrawal said.

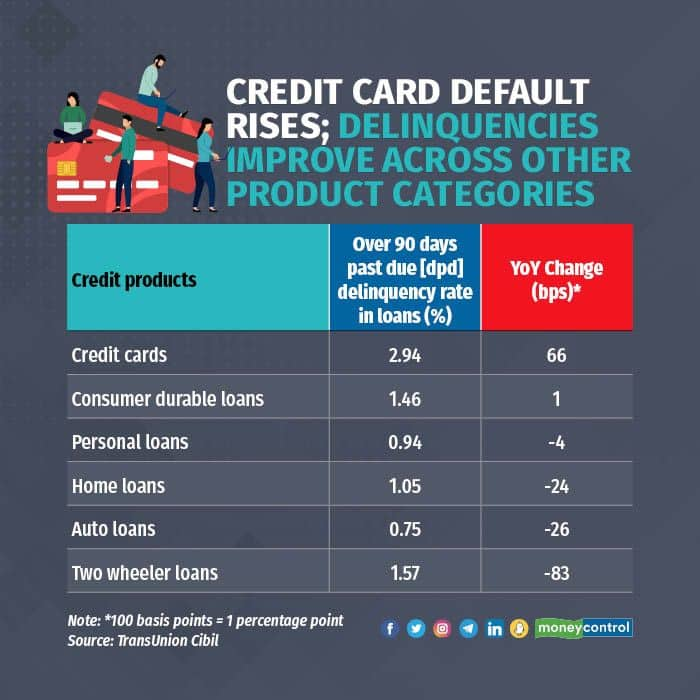

Credit card defaults rise

Credit card payment defaults increased in the quarter ended June 2023. For credit cards, over 90 days past due (dpd), the delinquency rate rose 66 basis points compared to the previous year to reach 2.94 percent (100 basis points equal 1 percentage point).

In other credit products, delinquencies have shown an improvement. Delinquency means nonpayment of a debt when due. This improvement suggests that consumers appear to be managing their credit repayments responsibly. For instance, the delinquency level in consumer durable loans remained almost flat, with the rate increasing by just 1 basis point to 1.46 percent (refer to graphic).

“Retail credit continues to remain on a strong and steady growth trajectory. While performance across credit products is stable, some segments require close monitoring to ensure sustained and long-term growth,” Kumar added.

ALSO READ: Why systematic withdrawal plans in MF work best for retirees

An explanation for the increase in credit card defaults could be the rapidly changing economic scenario, influenced by global challenges in some sectors and evolving consumer behaviour. “With the growing popularity of e-commerce and the rapid growth of online transactions, consumers are getting used to unprecedented ease in making purchases and availing finance. This, unfortunately, also presents a greater risk of impulsive buying using credit cards and a potential lack of financial discipline in repayment,” Agrawal said.

The number of unsecured loan payment defaulters in India increased to 32.9 percent in the personal loans segment as on April 21, 2023, compared with 31.4 percent over a year earlier. “This is due to a number of factors, including the rising cost of living, job losses, and the economic slowdown,” Manavjeet Singh, MD & CEO of CLXNS, a digital-first debt resolution platform, said. The debt collection industry can play a vital role in helping mitigate this situation by providing solutions to help defaulters repay their debts, he added. By that he means, offering flexible payment plans, and working with defaulters to help them get back on track financially.

“Credit card and loan issuers should prioritise responsible lending practices while ensuring that credit limits are granted in alignment with borrowers’ repayment capacity and reviewed over time in line with the prevailing economic scenarios,” Agrawal said. It is crucial to emphasise financial literacy programmes, educating consumers on responsible use of credit cards, and the importance of maintaining a healthy financial profile.

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!