Looking to apply for a home loan? Make sure to check your credit score first.

Banks covet borrowers with higher credit scores, offering them their best interest rates as well as other easy terms and conditions.

All new retail floating-rate home loans sanctioned since October 1, 2019 are linked to an external benchmark for determining interest rates. In the case of most banks, the repo rate happens to be the benchmark.

The effective interest rate – what is charged to the home-loan borrowers - is made up of the repo rate, the spread that the bank decides, and the credit risk premium, which is determined by the borrower’s credit score. Your credit score, therefore, could directly lead to a significantly lower interest rate burden.

Also read: RBI's rate pause: strategies to prepay your home loan

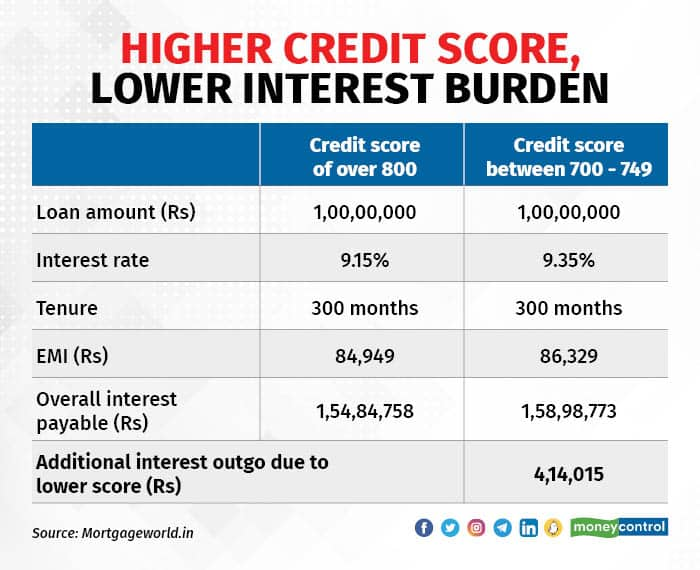

Higher credit scores mean lower loan rates

No loan or credit card application is approved without the lenders evaluating the borrower’s credit history and credit score.

Generally, the higher the score, the lower the chances of a default. For example, in the case of TransUnion CIBIL, the scores can range from 300 to 900.

“Most borrowers fall in the 700-800 range. A small percentage has scores higher than 800 and banks are keen on lending to this category,” says Vipul Patel, founder of Mortgageworld, a loan advisory firm.

A credit score is treated as an important metric as it indicates the borrower’s creditworthiness. Computed by credit information companies such as TransUnion CIBIL, Equifax, Crif Highmark, and Experian, the score depends on several factors including your repayment track record, delayed EMI payments, unpaid credit card dues, number of loans and credit cards in your portfolio or even loan applications, errors in credit reports and so on.

Put simply, a muddled repayment history – loan defaults or delayed EMI payments - could drag down your credit scores, which could mean the bank may reject your loan application or charge a higher rate of interest.

Also read: Moneycontrol's credit score check: Get quick, easy access to your credit score

For example, State Bank of India (SBI) offers a card rate of 9.15 percent to borrowers with a credit score of more than 750. If it's between 700 and 749, borrowers will have to pay 20 basis points more. One basis point is one-hundredth of a percentage point.

If it's lower than 700, then the rate applicable will be as high as 9.45 percent.

If you are looking to transfer your home loan from another bank to SBI, the rates start at 8.5 percent for those with credit scores of over 800 during the offer period that will end on June 30. It is 8.6 percent for credit scores between 700 and 749. SBI does not offer these concessional rates to borrowers with credit scores of under 700.

Also read: 'Many youngsters have an expensive lifestyle and are in debt. It’s a slippery slope'

Use credit score to negotiate better terms

Once a home loan contract is signed, banks cannot change the spread over the external benchmark for at least three years although they can offer rates with narrower or wider spreads to newer borrowers.

The Reserve Bank of India’s (RBI) external benchmarking rules allow banks to reset the credit risk component if their credit assessment indicates that the borrower’s credit profile has undergone a substantial change.

If it has deteriorated, your bank can revise your interest rates upwards and vice-versa. “If you have, over a period of time, managed to improve your credit score, approach your bank to renegotiate the rate applicable,” says Patel.

Chances are that to retain a creditworthy customer, your bank may agree to move you to a lower rate band.

Also read: Fallen into a credit card debt trap? Here are strategies to pay off debt

If your bank refuses to budge, you can consider transferring your loan to another lender. Many lenders waive the processing fee in such cases to attract borrowers with good credit profiles.

“You can always renegotiate in any case. Approach another lender, obtain a sanction letter, and renegotiate with your existing lender. They would want to retain borrowers with good credit scores and repayment track record,” says Raj Khosla, founder and managing director, MyMoneyMantra.

“Lenders spend a tidy sum to acquire new customers, so it is unlikely that will let go of someone with a good credit history,” adds Khosla.

Although housing finance companies are not bound by the external benchmarking mandate, competition is bound to force them to offer competitive rates to retain reliable customers.

HDFC, for instance, allows existing borrowers to switch to lower rates offered to newer customers upon payment of conversion charges. Currently, in the case of fully disbursed loans, the conversion fee is 0.25 percent or Rs 5,000 plus applicable taxes, whichever is lower.

Discover the latest business news, Sensex, and Nifty updates. Obtain Personal Finance insights, tax queries, and expert opinions on Moneycontrol or download the Moneycontrol App to stay updated!